Supply Concerns Recede, Oil Prices Fall

Supply Concerns Recede, Oil Prices Fall

In just two days

I have always maintained that tracking the sentiment of the market is a better indicator rather than looking at those complex graphs, charts with candle sticks and crisscrossed line across a screen to see where the markets are headed (I am not saying that it doesn’t matter, it does, but it isn’t the ONLY thing). For this purpose I recently tried to manifest my ideation in the form of a continuum (given below) where I place latest developments along bearish to bullish side. I have further bifurcated it into ‘recessionary’ and ‘geopolitical risk’ - the assumption being that these are the two key themes for 2022 (at least). Now that it is coming to an end, I need to rethink this categorization, however, I tend to think the thematic orientation of the next will be similar.

Recently, the narrative in oil markets have been subject to a tug of war where on one side we have people who believe in a recession induced destruction in demand while on the other one observers that are fretting over the lack of sufficient investment and foresee an oil supply crunch. I always maintained that at least in the shorter to medium term, the fears of a supply crunch are overblown and that recession will adversely effect oil demand.

I recently made this call on Asharq with Bloomberg.

I also wrote this for Oilprice.com two days ago highlighting the fact that demand destruction is a more serious concern than supply disruption.

Writing this on the morning of 19th November, 2022, oil prices are down more than $3 and might fall further. Why is this happening? Because “supply fears receded”.

This changed in two days. Did everyone just learn that there is enough supply or a new report came out? Nothing of this sort happened. The only thing changed was the collective market sentiment! This was bound to happen as from past 4 weeks there were signals of a bearish spell - this can also been seen in my Market Sentiment Tracker 2022 ( I reguarly cover this in my Monday Macro View for Primary Vision Network).

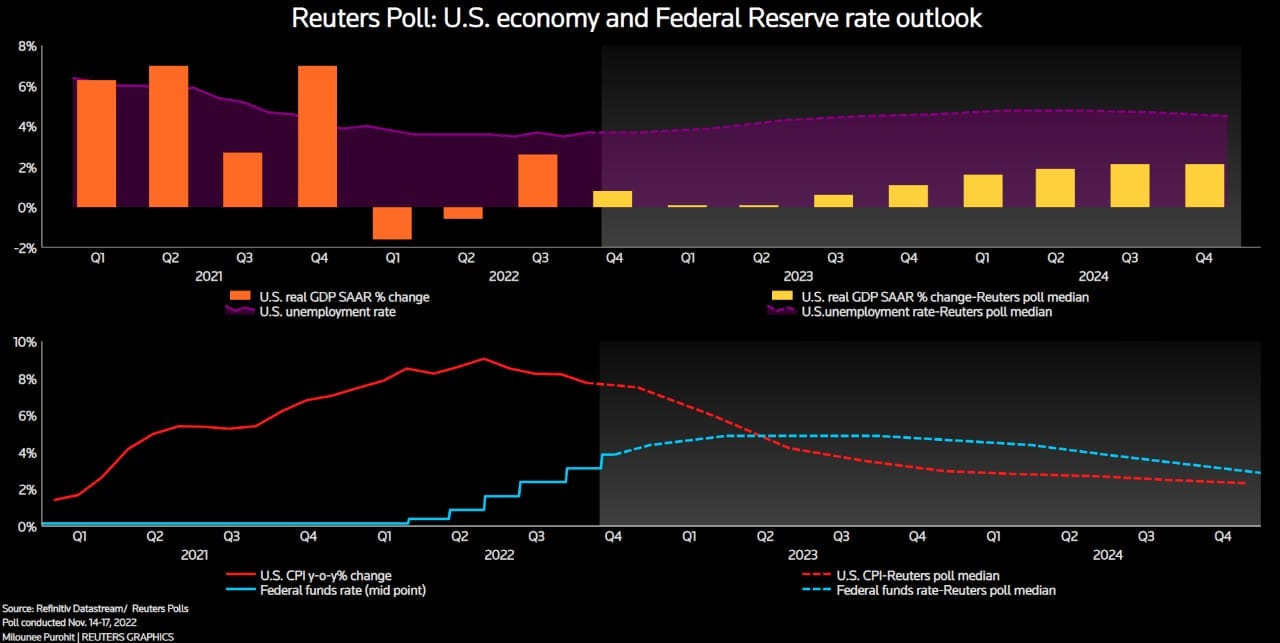

One of the most important signal (different from the “noise”) is to track the trajectory of U.S. interest rates. Recent comments by President of Reserve Bank of St. Louis, James Bullard, had the markets worrying.

Recent survey mentioned in Reuters shows even a more grim outlook. Most of the economists believe that interests rates will have to kept higher for longer and might peak only after touching 6 percent. As such unemployment rate is expected to increase 3.7 percent to 4.6 percent with the highest one being 5.9 percent.

So chances of a prolonged demand destruction are still there.

Shifting to the other side of the picture, there are many projects being planned in the oil and gas sector that will ensure the needs and demand of future are met. This can be highlighted by a recent report that speaks about the “frightening” growth in fossil fuels that can put efforts to curb carbon emissions under pressure. According to the report, the oil and gas sector has been piuring $160 billion since 2020 in exploration while 96 percent of E&P (exploration and production) firms have planned expansions. LNG expansion, for instance, is set to double in future.

I realize that one needs to investigate this further and there are many questions that can be asked in terms of assurance of an adequate supply:

Is the $160 billion more or less than what was being invested pre pandemic?

What is the level of investment that is required to meet world energy demand?

We know that global energy demand is set to increase, a fact now cemented by rising population that has hit 8 billion mark. What is going to be the speed of this increase?

So on and so forth.

But apparently and taking a bigger picture view, it is safe to say that fears of a supply crunch might be exaggerated. We need to buckle up for some serious correction in global asset valuations.

Enjoy the weekend!