Oil Prices Have Only Way to Go: DOWN

Oil Prices Have Only Way to Go: DOWN

Challenges continue to build up

Oil prices continue to tackle headwinds that are building up from past few weeks. In my last article I posited that prices will fall further - and they did. Brent has broken the psychological mark of $80 and at the time of writing is trading at $77.90. This is despite a more-than-expected inventory withdraw last week and another one expected today. However, in this environment where is there a lot of noise it is important to differentiate signals from it. Our estimates for 2023 and business decisions should be based on those signals and not the noise!

In terms of oil markets I believe that the case for a prolonged bear market is more than that of a bullish. This is indicated by the recent events in China where rising covid cases and falling manufacturing activity continues to put demand prospects from the second largest economy in the world at risk.

Source: Monday Macro View, Primary Vision Network

Mark Rossano has spoken at length about the latest economic indicators coming out of China and none of them are encouraging. I highly suggest that you go and check out this segment of the ECON show. But to build up on my argument, focusing on China is important because it is one of the largest consumers of oil and any news regarding a slowdown in the country can shift global market sentiment which is already near its tipping point - to be tipped into a bearish territory.

Source: ECON Show, Primary Vision Network

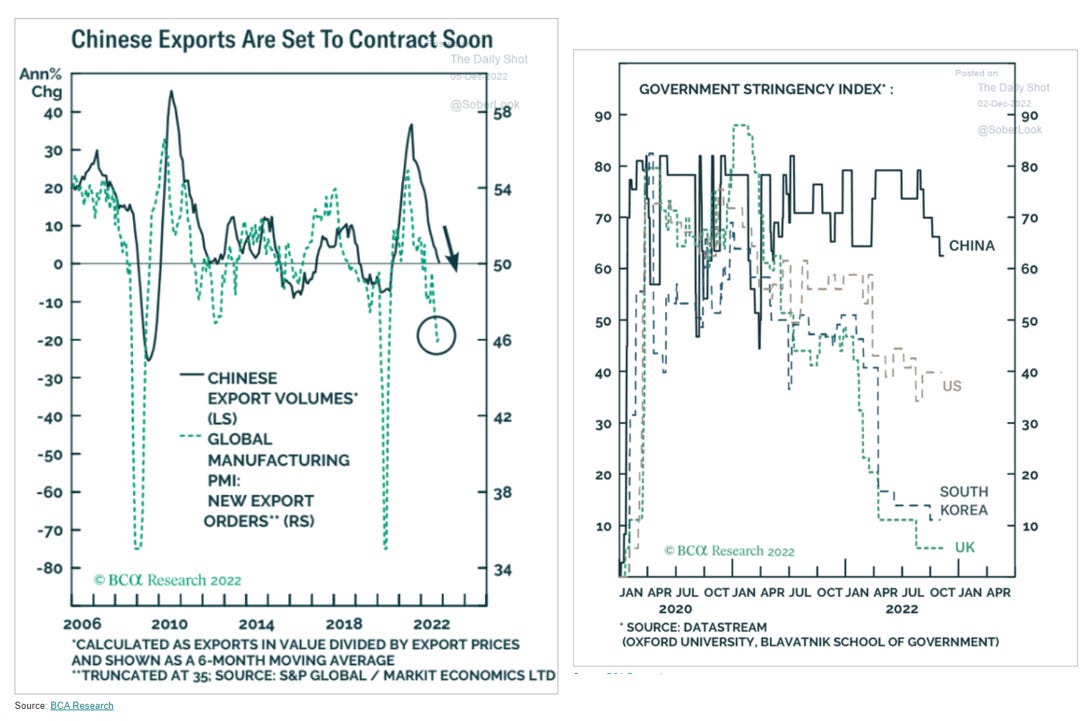

Things at the export front are also not good:

Source: ECON Show, Primary Vision Network

There are many other interesting charts, all showing the same picture. As we step into 2023, China will continue to be in focus as the million dollar question - whether its economy will revive or not?

Besides downside for oil demand concerning China, there are other indicators as well. Consider for example, Saudi Arabia cutting its OSP to Asia to a 10 month low! Saudi Arabia cut the price of its benchmark Arab Light oil by $2.20 per barrel and $1.80 to Europe.

China has also cut its gasoline and diesel retail prices in a hint of weaker domestic demand. It is expected that China’s oil consumption can fall between 200,000 bpd to 300,000 bpd in the months ahead despite easing of the lockdowns.

Dollar has managed to retain its strength as recent data showed some optimism regarding US economy. The ISM’s (Institute for Supply Management) non-manufacturing PMI improved to 56.5 from 54.4 highlighting that the services sector is performing well. The sector contributes two-thirds to the country’s economy.

In terms of global economy and recessionary fears the condition continues to worsen. Recent outlook by Blackrock looks at the future with some pragmatic lens.

Source: Blackrock, Global Investment Outlook 2023

We will continue to see bearish factors piling. The shift in global sentiment is not a recent one but it was present since the start of the year. Gradually the over-representativeness of good news fizzled out and we saw clearly what lies ahead. 2023 is going to be a redux of 2022 - it might get uglier but not better.

If we take global economy as a ship then the message should be to brace yourself - there might be some icebergs ahead.