Oil Markets, IMF Outlook and Some Readings

Oil Markets, IMF Outlook and Some Readings

Conflicting signals and misplaced optimism

The recent week was full of interesting reports. IMF gave us a reality check - much needed - however, they minced their words in terms of what we really are looking at when exploring the prospects of global economic growth (or shoud we say recovery). There was some estimates by OPEC+ and IEA as both gauged the future of oil demand and supply with the former sticking to the reality taking in a bigger picture view of the global macroeconomic indicators that seem to be screaming recession as compared to the latter that still has some hope (misplaced, I must mention) in terms of a resurgence in oil demand.

The International Monetary Fund (IMF) has released its latest World Economic Outlook report, stating that the global economy is heading for its weakest growth since 1990. The IMF expects global growth to be around 3% in five years’ time, the lowest medium-term forecast in the past three decades. The report cited the progress of economies like China and South Korea in increasing their living standards, slower global labour force growth, and geopolitical fragmentation as the reasons behind the weaker growth prospects. The IMF also expects global growth of 2.8% this year and 3% in 2024, slightly below the fund's estimates published in January, with a cut of 0.1 percentage point for both years.

The IMF highlighted several reasons for the anemic outlook, including the tight policy stances needed to bring down inflation, fallout from the recent deterioration in financial conditions, ongoing war in Ukraine, growing geoeconomic fragmentation, commodity price spikes, and new financial stability concerns. Looking at some of the regional breakdowns, the IMF sees the United States economy expanding by 1.6% this year, the eurozone growing by 0.8%, and the United Kingdom contracting by 0.3%. China's GDP is expected to increase by 5.2% in 2023, and India's by 5.9%, while the Russian economy is seen growing by 0.7% this year, having contracted by over 2% in 2022.

The IMF warned of the potential for banking turmoil after a number of banks failed in March, causing volatility across global markets. The report noted that the recent financial sector stresses must be contained to prevent contagion, and the IMF sees this as a significant risk to global financial stability. Higher interest rates, raised by central banks battling to bring down stubbornly high inflation, are hurting companies and national governments with high levels of debt. The IMF expects global headline inflation to drop from 8.7% in 2022 to 7% this year, as energy prices come down, but core inflation, which excludes volatile food and energy costs, is expected to take longer to fall.

Key Insights:

The IMF expects global growth to be around 3% in five years’ time, the lowest medium-term forecast in more than 30 years, with the United States economy expanding by 1.6% this year and the eurozone growing by 0.8%, while the United Kingdom is seen contracting by 0.3%.

The recent financial sector stresses must be contained to prevent contagion, and the IMF sees this as a significant risk to global financial stability.

Higher interest rates, raised by central banks battling to bring down stubbornly high inflation, are hurting companies and national governments with high levels of debt, which could result in a hard landing, particularly for advanced economies.

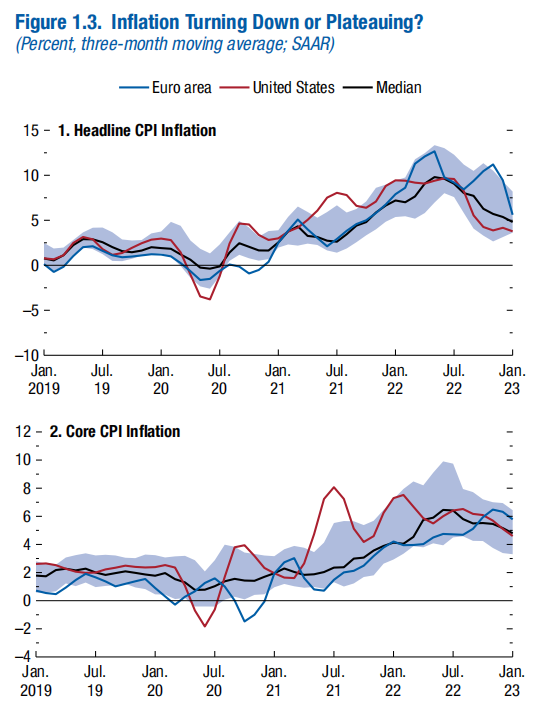

Here is what IMF’s WEO says about inflation:

“Higher for longer” interest rates to “address sticky inflation”. The charts show inflation coming down in future. But one thing that we need to discuss is the impact of this on the labor markets and overall economy. The question: is it possible to do it without inducing a recession?

Now something on the oil markets. The oil markets have seen a recent rise in prices due to OPEC+'s announcement of new voluntary production cuts set to take effect in May. The organization has acknowledged potential downside risks to summer oil demand, which was previously noted by me in a recent article for Oilprice.com.

OPEC has cited several factors contributing to these risks, such as building oil inventories, less tight product balances than the previous year, challenges to global economic development, and a decline in global refining intake of crude. Despite these challenges, OPEC has maintained its forecast that oil demand will rise by 2.3% in 2023.

The voluntary production cuts agreed upon by OPEC+ amount to 3.66 million bpd, equal to 3.7% of global demand. OPEC's March output fell by 86,000 bpd to 28.80 million bpd, with declines in Iraq and Angola. The report also indicated that OPEC needs to pump 29.3 million bpd in 2023 to balance the market, which is steady from previous estimates. However, the report's release led to a weakening of oil prices, with Brent crude falling below $87 a barrel.

In contrast, the International Energy Agency (IEA) predicts that global oil demand will reach a record high of 101.9 million barrels per day (bpd) in 2023, representing an increase of 2 million bpd. This growth is largely due to a surge in Chinese consumption following the lifting of COVID restrictions, with jet fuel demand accounting for 57% of the growth. Analysts suggest that rising Chinese demand is helping to offset warnings from OPEC.

The IEA has warned that the OPEC+ decision could harm consumers and the global economic recovery, as it is likely to lead to inflated prices for basic necessities. The agency also predicts that global oil supply will decrease by 400,000 bpd by the end of 2023, with a production increase of 1 million bpd expected outside of OPEC+.

Bearish Case for Oil

Despite the recent retracement in oil prices I maintain my bearish case for oil. Apart from the global economic indicators and chances of a recession demand from China remains weak or not as strong as was previously expected. Clyde Russell for Reuters in a recent article highlight how there has been an increase in imports from China but its export sector registered even a further increase suggesting weak domestic demand.

IMF’s report, estimates about higher interest rates, lukewarm Chinese demand and OPEC+ production cut all make for a strong case for another fall in oil prices.

This was endorsed by Ed Morse of Citi group:

Apart from these news, this chart relate to my previous substack and is on point regarding the dominance of dollar in global financial system:

This was a very nice coverage about Pakistan and what IMF has to say about it:

Link: https://www.aljazeera.com/economy/2023/4/12/imf-forecasts-pakistans-economy-to-slump-inflation-to-rise

A very nice article that relates to our discussion above regarding oil markets:

Link:

Link: https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/041223-asian-refiners-back-opec-cut-but-fret-over-regional-oil-demand-on-weak-macroeconomics

If all of this reading makes you tired, this will be helpful:

Happy Sunday and Happy Reading!