Oil Ban, Interest Rates and Recession

Oil Ban, Interest Rates and Recession

What's Going On Here? The need for Second Order Thinking!

The book I am reading at the moment is not only very interesting but also highly relevant to the contemporary times - in fact it captures the financial zeitgiest of post pandemic world. The book’s title is “Radical Uncertainty” with a subtitle “Decision making for an unknowable future”. Among numerous insights and lessons the book hold, one of them (and the overarching theme of the whole book as well) is the idea of asking “What’s going on here?”. The writers rightly point out that many decision makers give too much importance to models, algorithms and numbers without truly appreciating the wider context the problem is operating in (I’ll do a detailed review of the book next week to explain it in detail). That leads to myopic decisions which often yield unintended consequences.

With an impending ban on Russian oil and gas, rising interest rates, and calls for recession taking hold - I will try to share my answer to “what’s going on here?”.

Recently, European Union has categorically shared its plan to wean itself off of Russian oil and gas. In a recent round of sanctions it was made clear that the bloc will stop using Russian oil by the end of the year. While plans are set to reduce demand of Russian gas by two thirds after 2022. What’s worrisome is the fact that as per the new directive (and if it is to be implemented) Russia will find it very hard to explore new markets for its energy exports. Below is an excerpt from the directive by EU as mentioned by Javier Blas in his recent article for Bloomberg.

“It shall be prohibited to purchase, import or transfer, directly or indirectly, crude oil and petroleum products, if they originate in Russia or are exported from Russia. It shall be prohibited to provide, directly or indirectly, technical assistance, brokering services, financing or financial assistance, or any other services related to the prohibition in paragraph 1.

It shall be prohibited to transport, including through ship-to-ship transfers, to third countries crude oil and petroleum products which originate in Russia or have been exported from Russia, by any vessel registered under the flag of a Member State or owned, chartered, operated or otherwise controlled by a national of a Member State or any legal person, entity or body incorporated or constituted under the law of a Member State.””

Now from the standpoint of curbing Russian finances in order to stall or thwart its warmongering in Ukraine this sounds like a great plan. However, there can be serious unintended consequences as well.

Every policy has an immediate effect - which might be the desired result. However, problems arise when we fail to take into account the second order thinking: You got hungry and wanted to eat a beef burger, and you did. But what you failed to take into account its effect on your cholestrol levels which are dangerously high! Similarly, we want to punish Russia for its intrigues in Ukraine, we choke its main source of revenue i.e. energy exports. However, what we don’t see is that the world at large has already been fighting an energy crisis (especially the EU) and with inflation at its highest levels in several countries and OPEC+ already producing 1.5 mbpd less than what they used to, such an action can be a recipe for disaster for the global economy.

EU depends for a quarter of its oil and more than 40 percent of gas from Russia. As such both have an interdependence on each other (EU for its energy, Russia for its revenue). However, what are the alternatives for both?

According to different estimates, out of 5 mbpd of Russian oil exports, only 2 mbpd day can be replaced that too only if OPEC+ raises it output to maximum! There are other options such as Venezuela, Iran, Libya, Azerbaijan, Algeria but each country has their own set of problems: some are infrastructural and some political and in most of the cases a mixture of both. Similarly, in terms of gas, Qatar is an option but it is on record saying that no one country can replace Russia as a source of gas supply to EU. Also, most of Qatar’s gas is headed towards Asia with only 10-15 percent left for Europe.

For Russia, Asia can be its largest market but lukewarm demand from China (one of the largest consumers of oil) may create further problems. As sanctions bite in and Russia is gradually exluded from the international financial system, China has started to avoid dealing with the country’s crude. According to Vortexa, “loadings of Urals in April with a firm destination to China totalled 75kbd, down nearly 50% from Q1.” India is purchasing crude from Russia but is doing so at a steep discount (at 20 percent). Other countries will try to do the same which will create a revenue shortall for Russia. As per an article in S&P Global Platts, oil revenue in Russia have fallen by almost $380 million per day down from $430 million per day back in 2021.

That’s the goal, right?! But, what about the second order thinking? How will all of this impact the world especially the developing countries? With OPEC+ output already down by 1.45 mbpd and concerns regarding insufficient spare capacity and an impending supply crunch are bolstering.

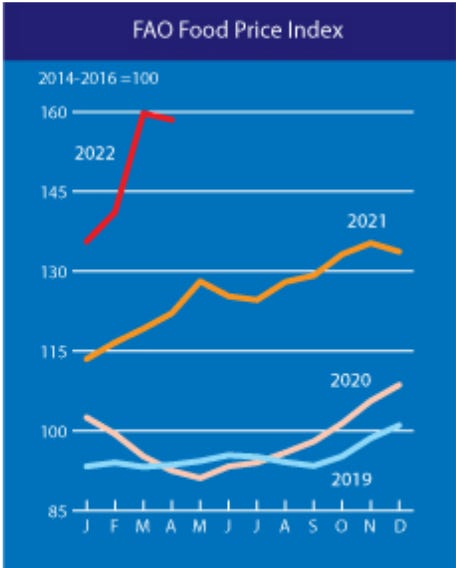

Dollar index reached its highest in two years in the past few days and Fed increased its interest rates by 50 basis point - the largest since 2000s. This bring us to the developing world where a record amount of debt is already putting immense pressure on nationla exchequer as imports are getting expensive along with debt servicing while inflation creeps higher and food prices are off the charts. Sri Lanka was just one example where a Balance of Payment crisis set off a series of events culminating into soveriegn default, state of emergency and country-wide protests. Other countries might follow suit (I wrote about it that how this will not stop at Sri Lanka for The National Interest). Pakistan is facing similar issues as the recent ouster of PM Imran Khan has aggravated political uncertainty and the incumbent government will be presenting a budget very soon with the largest ever fiscal deficit in the history of country (I have written about it in more detail here for The Diplomat Magazine).

In such a scenario, one may ask: what is the solution? Of course, from an idealistic point of view, we need some sort of de-escalation between West and Russia and it remains the most important factor in introducing some political and economic stability in the world. However, from a realist and realistic point of view that doesn’t seems to be the case. That said, an outright ban on Russian oil that too this swiftly, in the current economic context the world is operating in, can prove to be extremely harmful for everyone. I have spoken to Captial.com on how this can even take oil prices beyond $200 if certain developments take place.

This is a developing story and I will be writing more on this. Until then Happy Weekend!